Mudra Kawach – Financial Strength for Every Indian

Mudra Kawach is an important financial support initiative of the IPV Bharat Project, designed with a mission to make every Indian citizen financially stronger and more secure in life. In today's world, financial challenges can arise anytime—whether it is for education, medical emergencies, business needs, family responsibilities, or unexpected situations. Mudra Kawach aims to create a community-driven support system where members can receive timely financial assistance when they need it the most.

The vision of Mudra Kawach is to build a strong network of responsible and supportive members across India who contribute together and help each other during financial difficulties. This initiative works on the principle of collective strength, transparency, and long-term social support.

Through the Mudra Kawach system, members of the IPV Bharat Project can request financial assistance according to their membership contribution and project policies. The system is designed to ensure that members are not left alone during financial challenges and can receive support from the growing IPV Bharat community.

Mudra Kawach is not only about financial assistance but also about building a secure and supportive ecosystem where members help each other grow and overcome difficulties. With time, the IPV Bharat Project aims to strengthen this system and expand its reach so that more people across India can benefit from it.

Members who join the project become part of a larger mission that focuses on complete life security through 30 different service sections, including financial support, employment support, legal help, medical support, and many other social welfare services.

The financial assistance provided through Mudra Kawach is structured in a way that encourages responsible participation and cooperation among members. When members repay previously availed assistance, their eligibility for higher assistance may increase according to project policies.

Another key feature of Mudra Kawach is the community growth model, where members can also receive referral benefits by introducing new members to the project. This helps expand the network and increases the overall strength of the support system.

The IPV Bharat Project encourages all members to actively participate in spreading awareness about the project and its social objectives through digital platforms such as Facebook, Instagram, WhatsApp, Telegram, LinkedIn, YouTube, and other social networks. This collective participation helps the project grow faster and reach people who genuinely need financial support.

Mudra Kawach is built on the belief that when people support each other, financial challenges become easier to overcome. By becoming a member of the IPV Bharat Project, individuals join a long-term movement dedicated to building a financially secure and socially supportive India.

Terms & Conditions

IPV Bharat Project – Membership Policy

1. Eligibility

Membership of the IPV Bharat Project is available only to Indian citizens. The applicant must be 18 years of age or above to become a member.

2. KYC Requirement

Basic KYC information, such as name, address, identity proof, and bank details, is mandatory for membership registration.

3. Membership Contribution

Membership of the IPV Bharat Project can be taken with a contribution ranging from ₹100 to ₹1,00,000 once in a lifetime. This membership contribution is non-refundable.

4. Payment Method

Membership contributions must be paid only through the official website payment gateway options.

5. Service Coverage

Members will receive life support and protection services through 30 different service sections of the IPV Bharat Project, which will be activated gradually over the next 10 years.

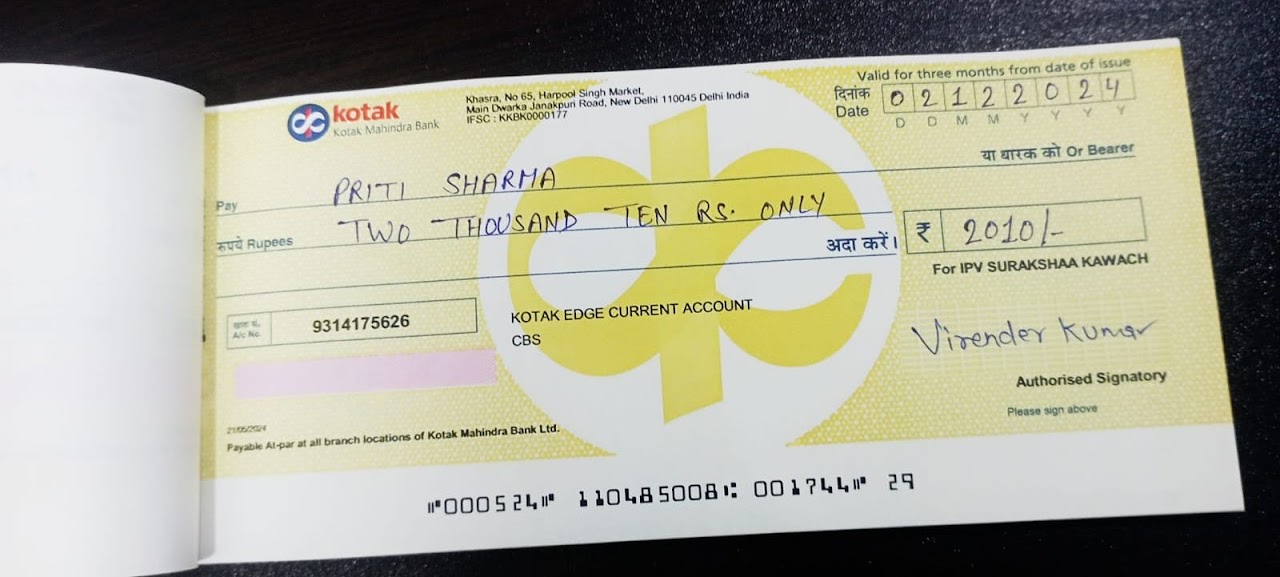

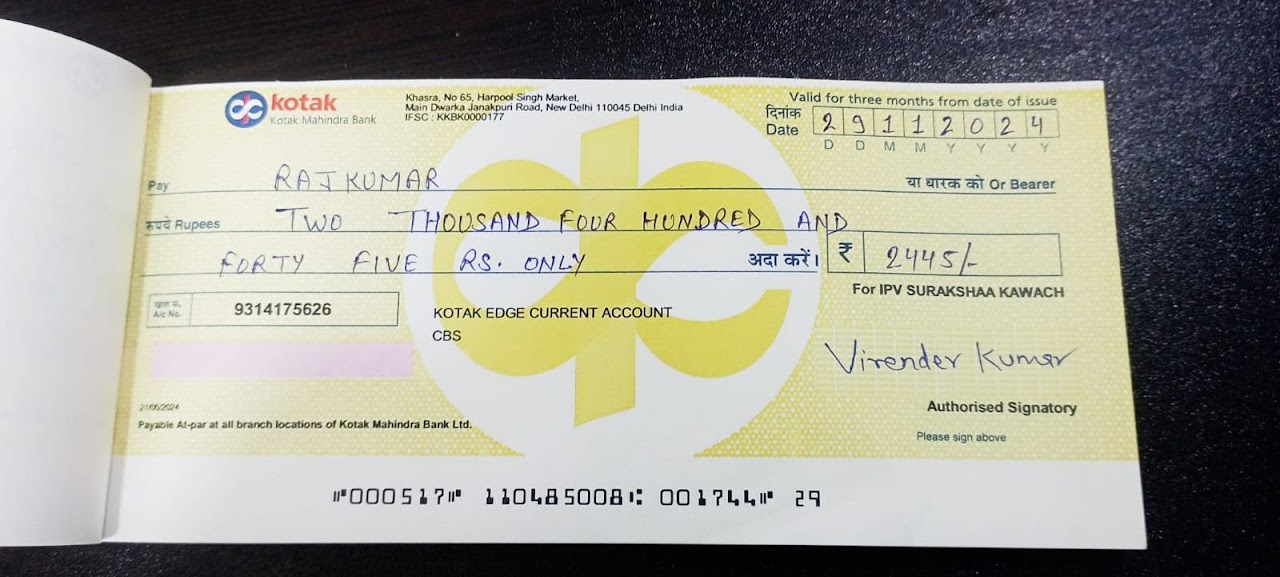

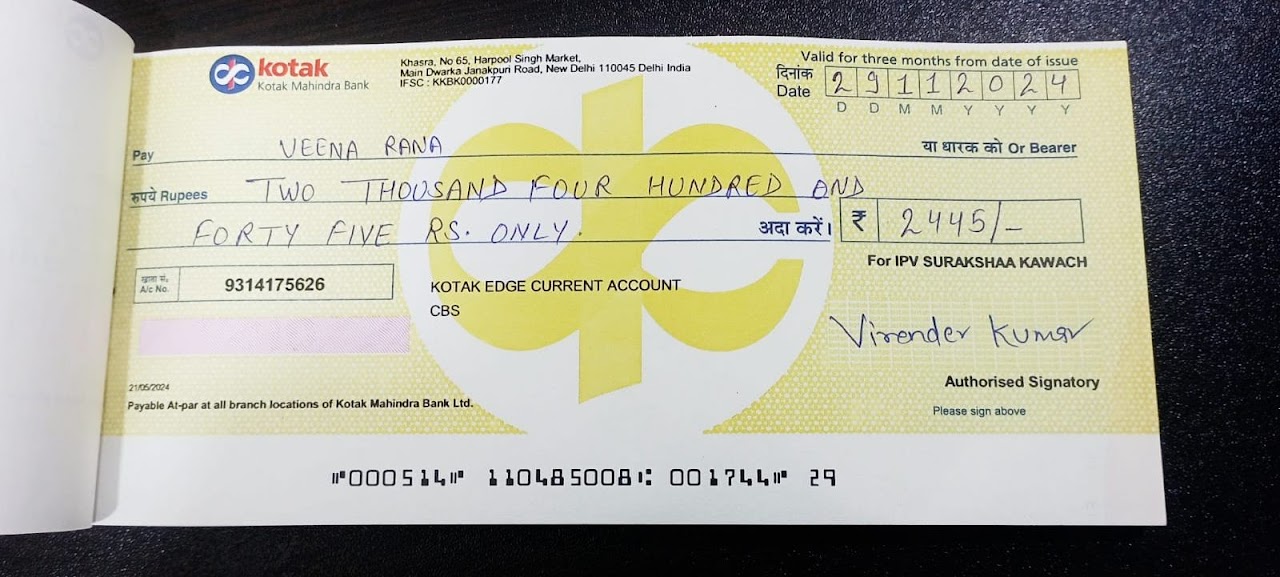

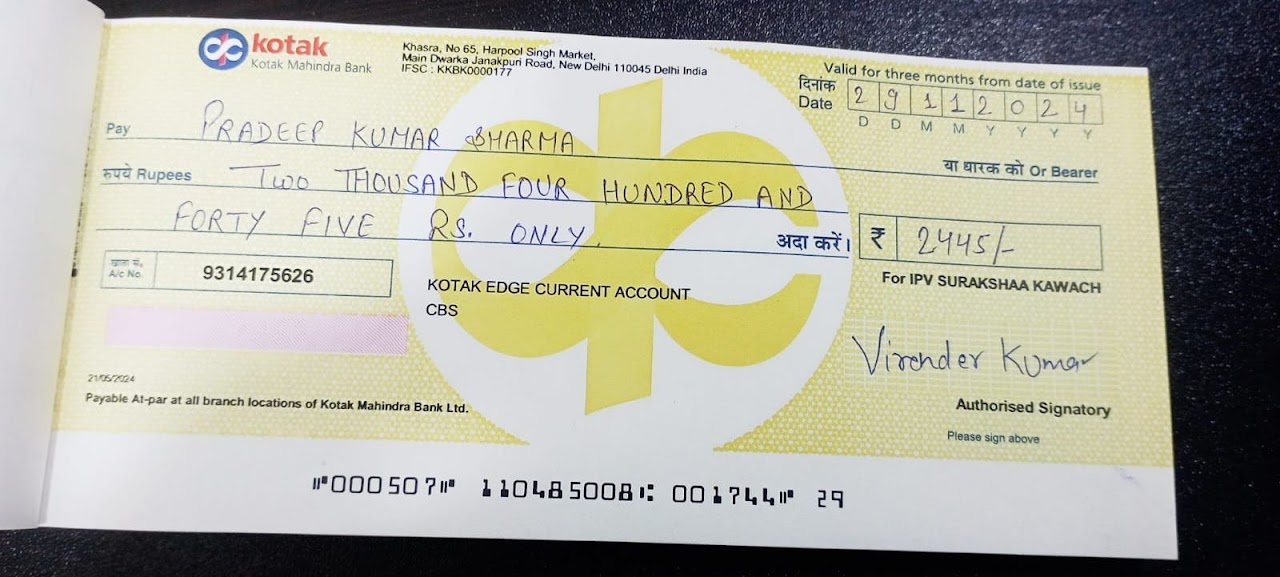

6. Financial Assistance Facility

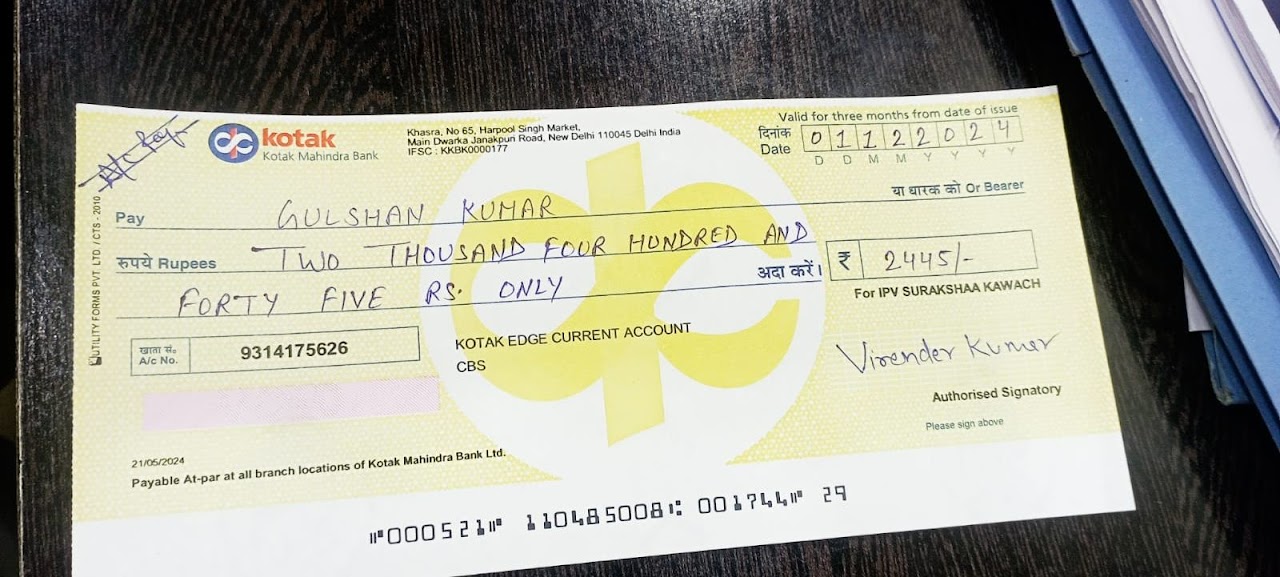

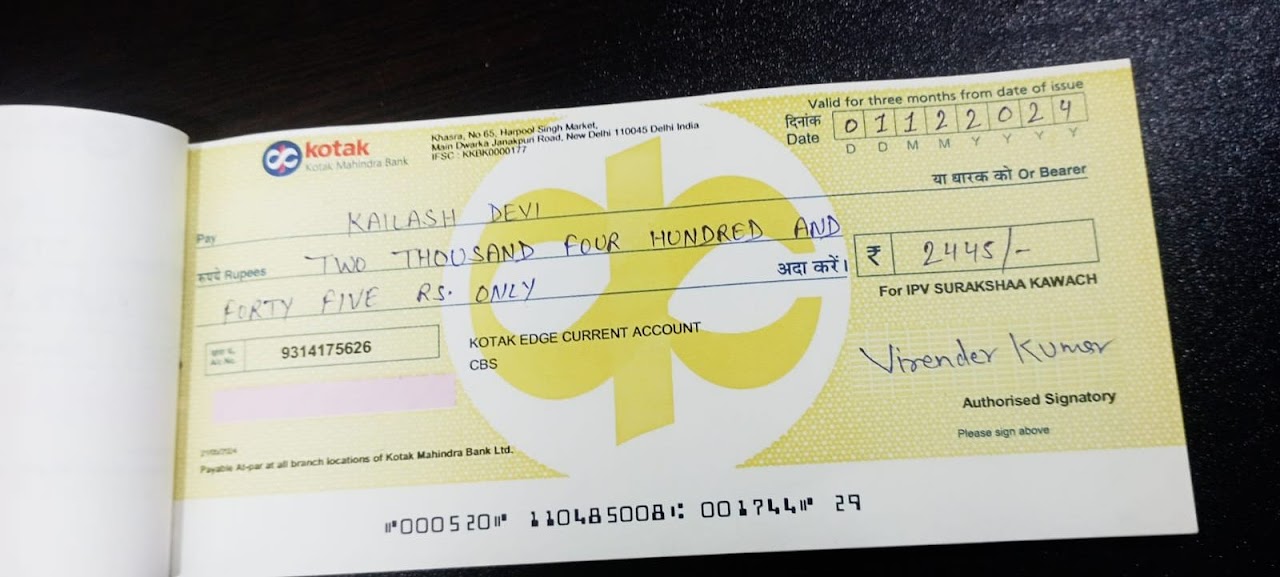

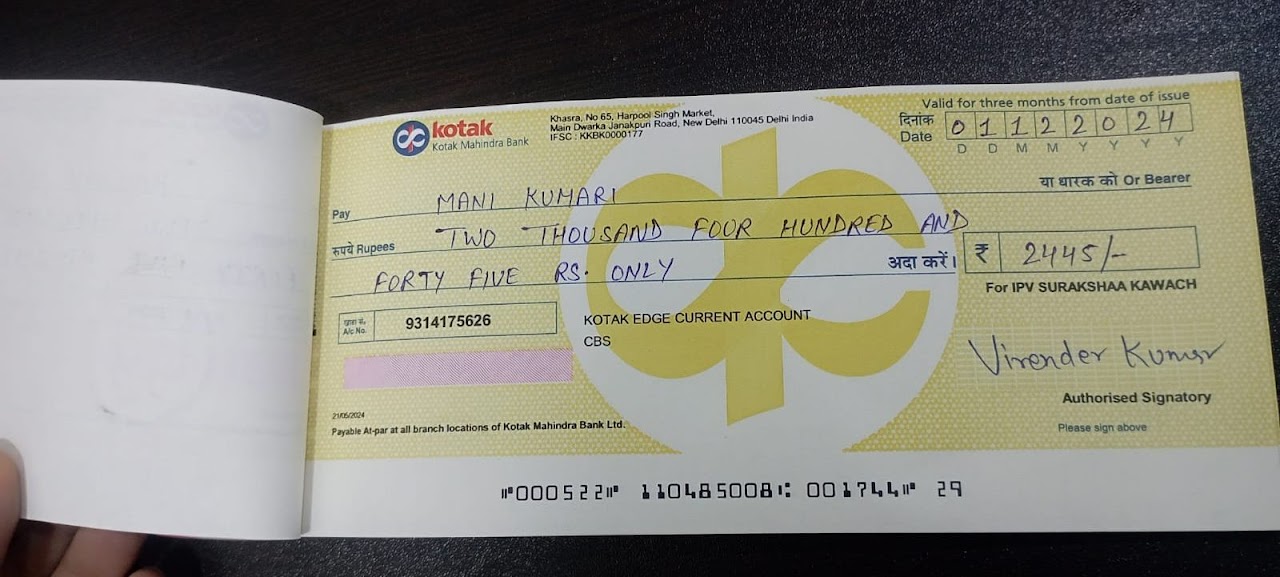

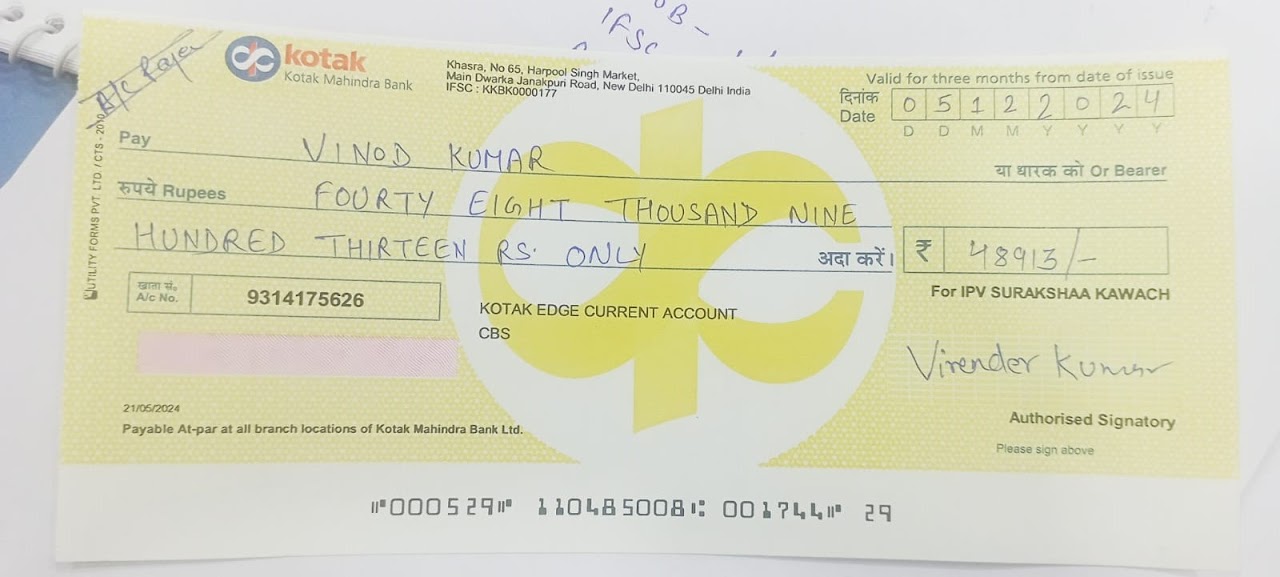

Members may receive financial assistance services based on their membership contribution. The assistance amount may increase after repayment of previously availed assistance as per project policy.

7. Request and Disbursement Process

Members must raise a request for financial assistance. After the request is raised, the assistance amount may be disbursed within 30 days, subject to approval and availability of funds. The repayment tenure will generally be up to one year.

8. Auto Assistance Support

The project may provide internal support systems that help members in repaying the financial assistance as per the project structure.

9. Referral Benefit

Members may receive 10% referral benefit based on the membership contribution of the members referred by them, according to the project policy.

10. Request Submission Process

For financial assistance, members must submit their request on WhatsApp number: 9354679155 along with the screenshot of their My Income Page.

11. Member Participation

Members are expected to promote the social objectives and activities of the IPV Bharat Project by sharing its videos, pages, and services on social media platforms such as Facebook, X (Twitter), Instagram, LinkedIn, WhatsApp, Telegram, and YouTube.

If a member remains inactive on the website or project activities for a long period, their benefits may be temporarily stopped.

12. Community Support

The project aims to build a supportive community. Members are encouraged to help and support other members who may be facing difficulties in life.

13. Termination / Suspension Clause

Membership may be terminated or suspended in the following situations:

• Providing false or misleading information

• Involvement in illegal activities

• Misuse of trust services or project facilities

• Violation of the rules or policies of the project

In such cases, the member’s benefits may be discontinued.

14. Liability Disclaimer

The IPV Bharat Project does not guarantee any financial return or profit. Any assistance provided under the project depends on available resources, policies, and approval procedures.

15. Data Privacy

Personal information provided by members will be used only for the activities and operations of the project and trust. Such information will not be shared with third parties without permission, except where required by law.

16. Governing Law

The membership and services of the IPV Bharat Project shall be governed by the laws of India. Any dispute arising from membership will fall under the jurisdiction of the courts where the trust’s registered office is located.

CLICK HERE TO REGISTER AND START THE FINANCIAL GROWTH BENEFITS

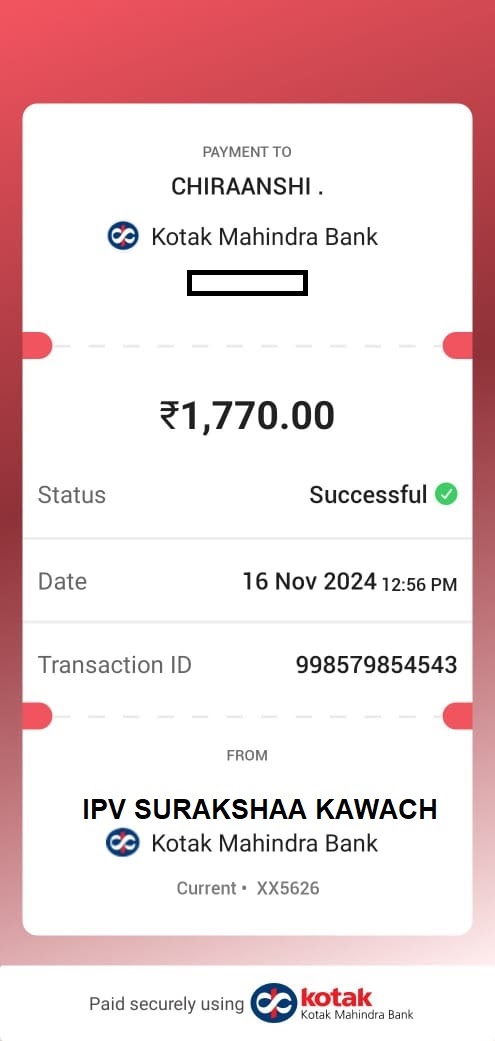

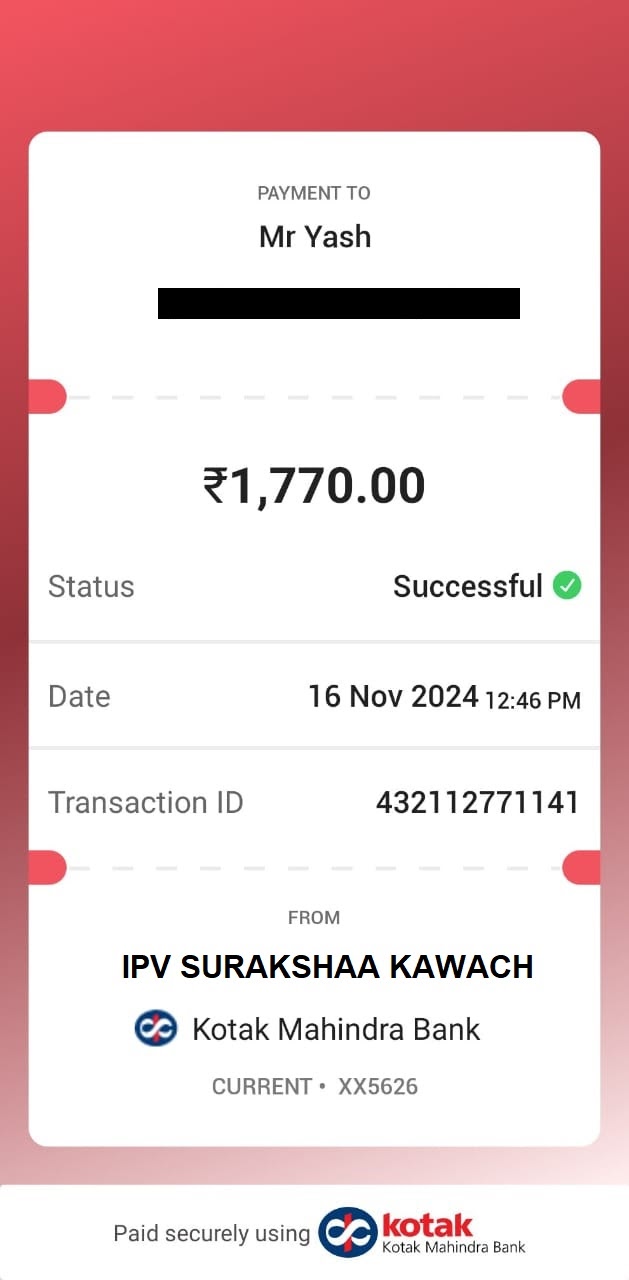

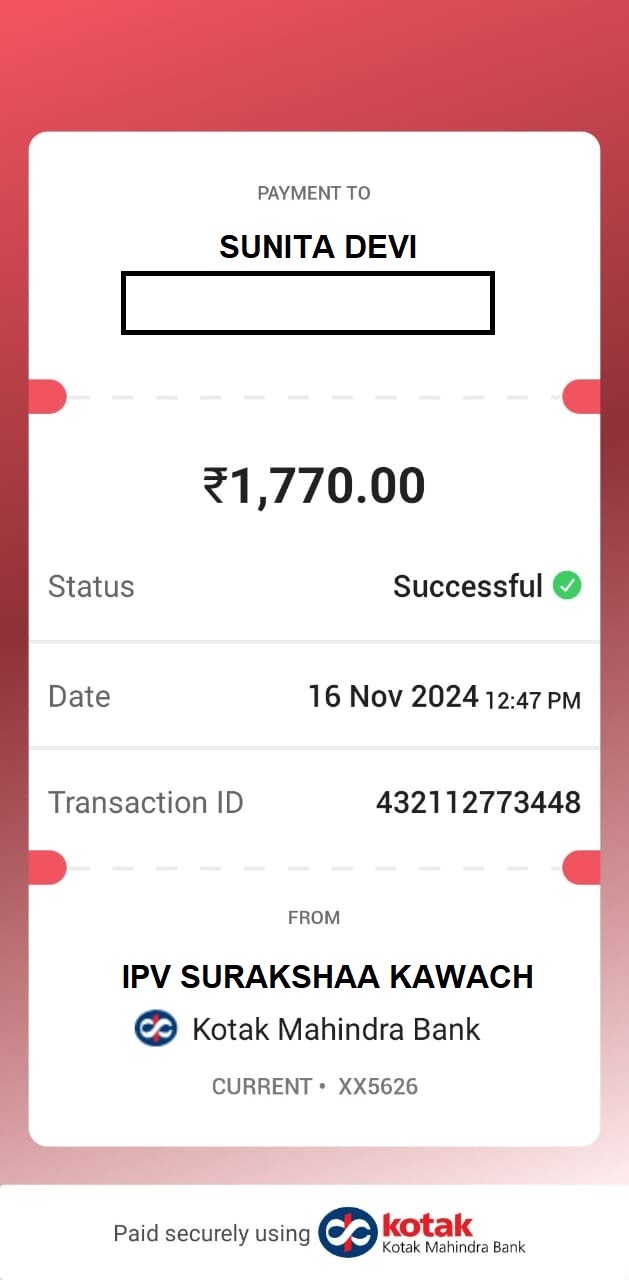

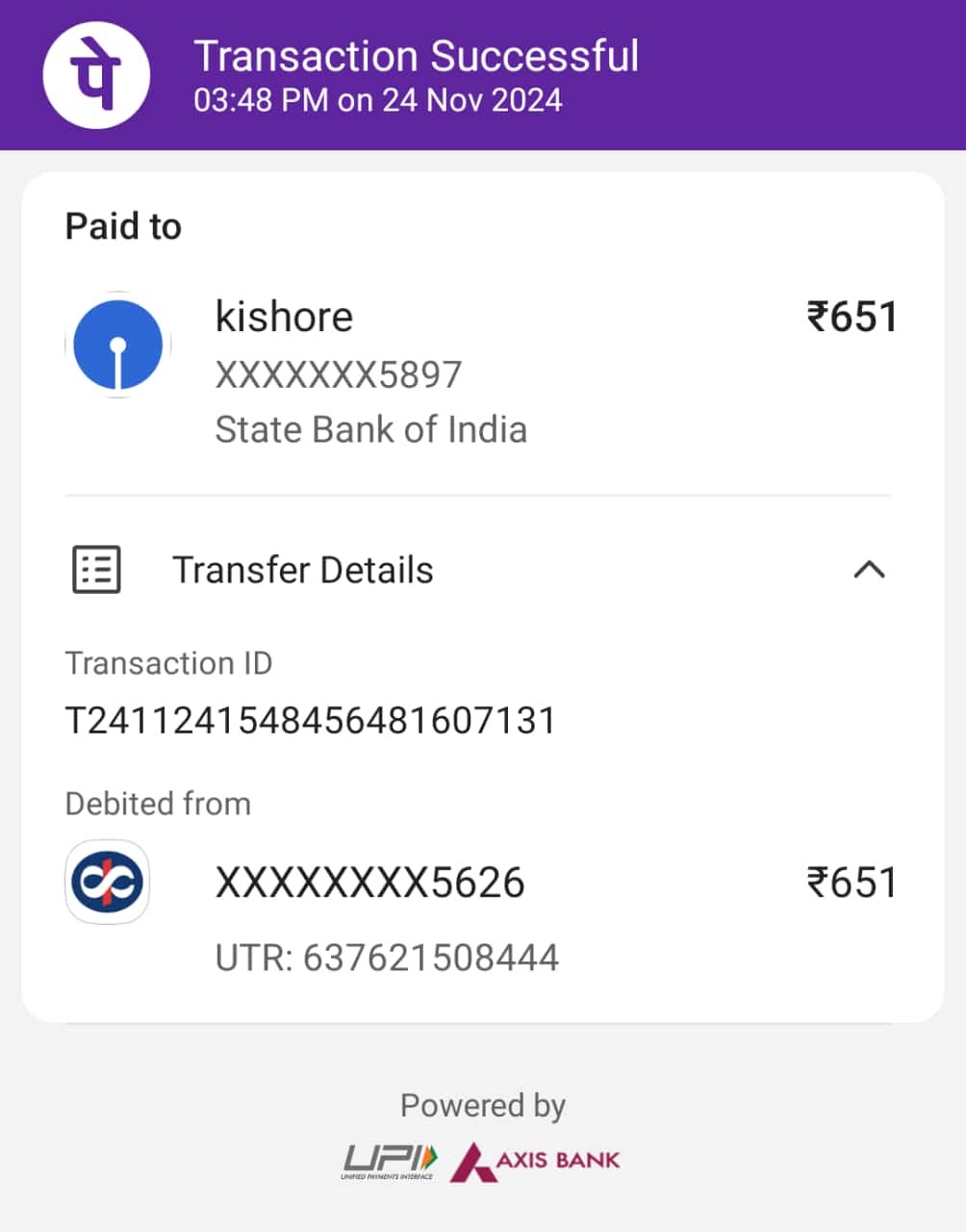

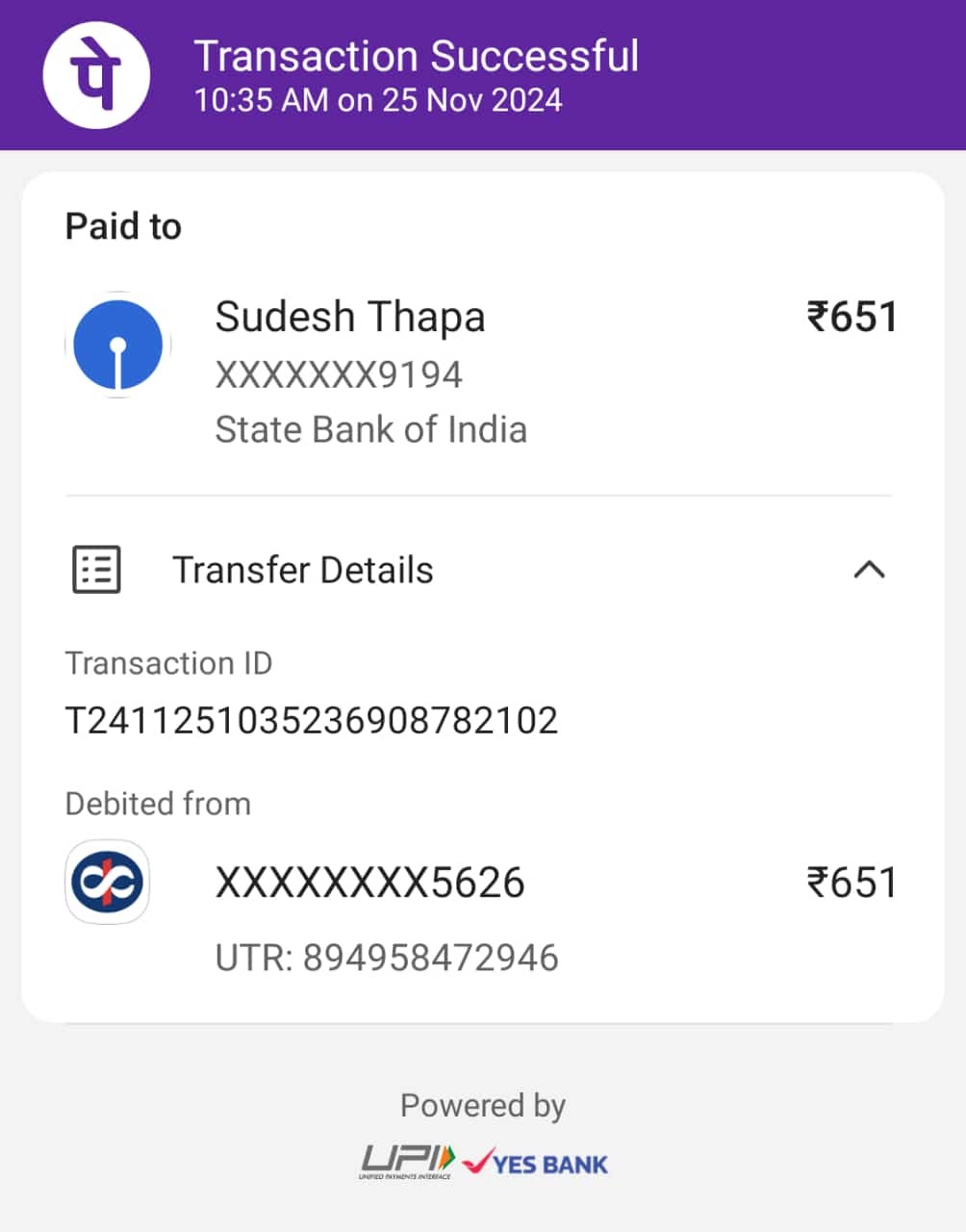

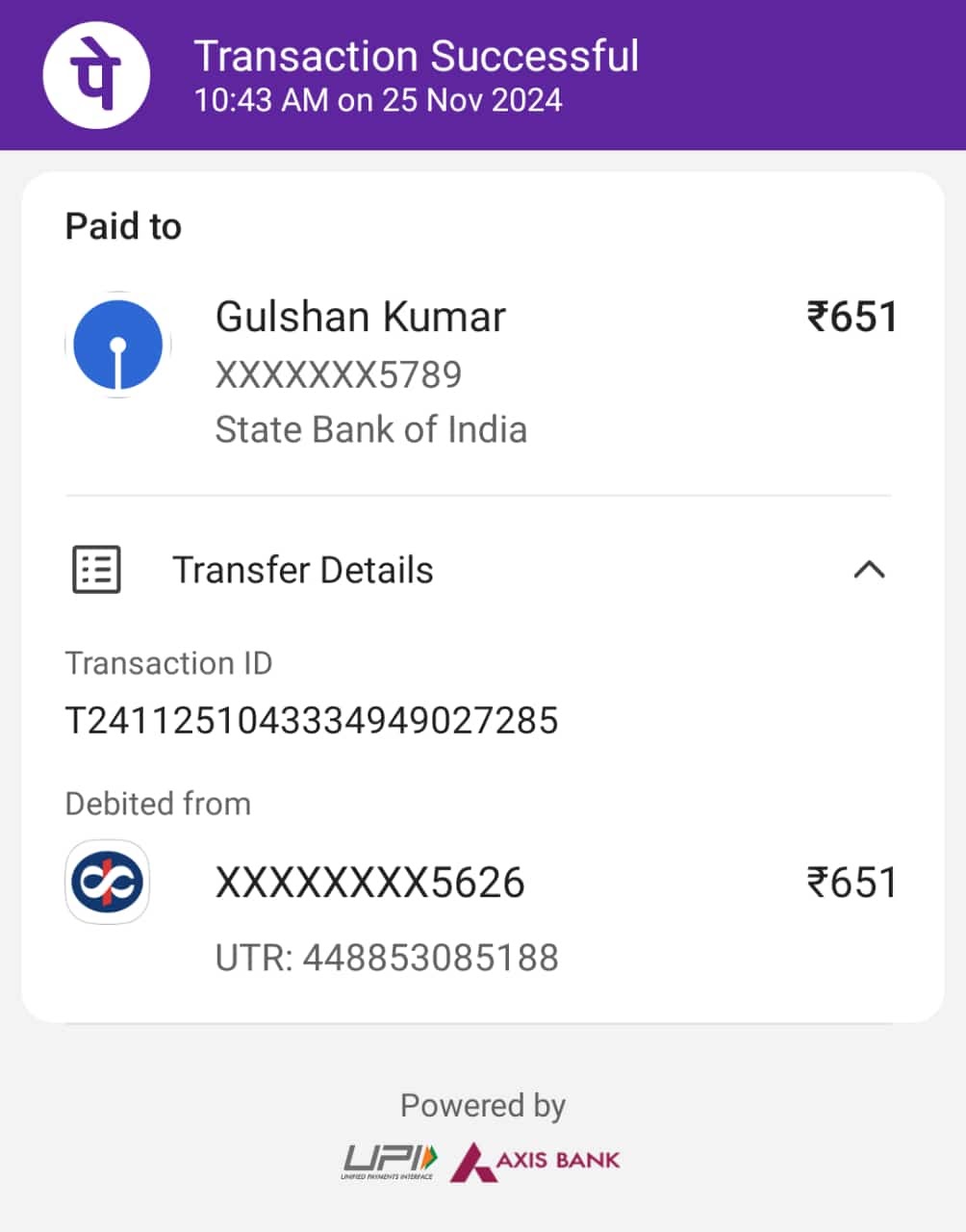

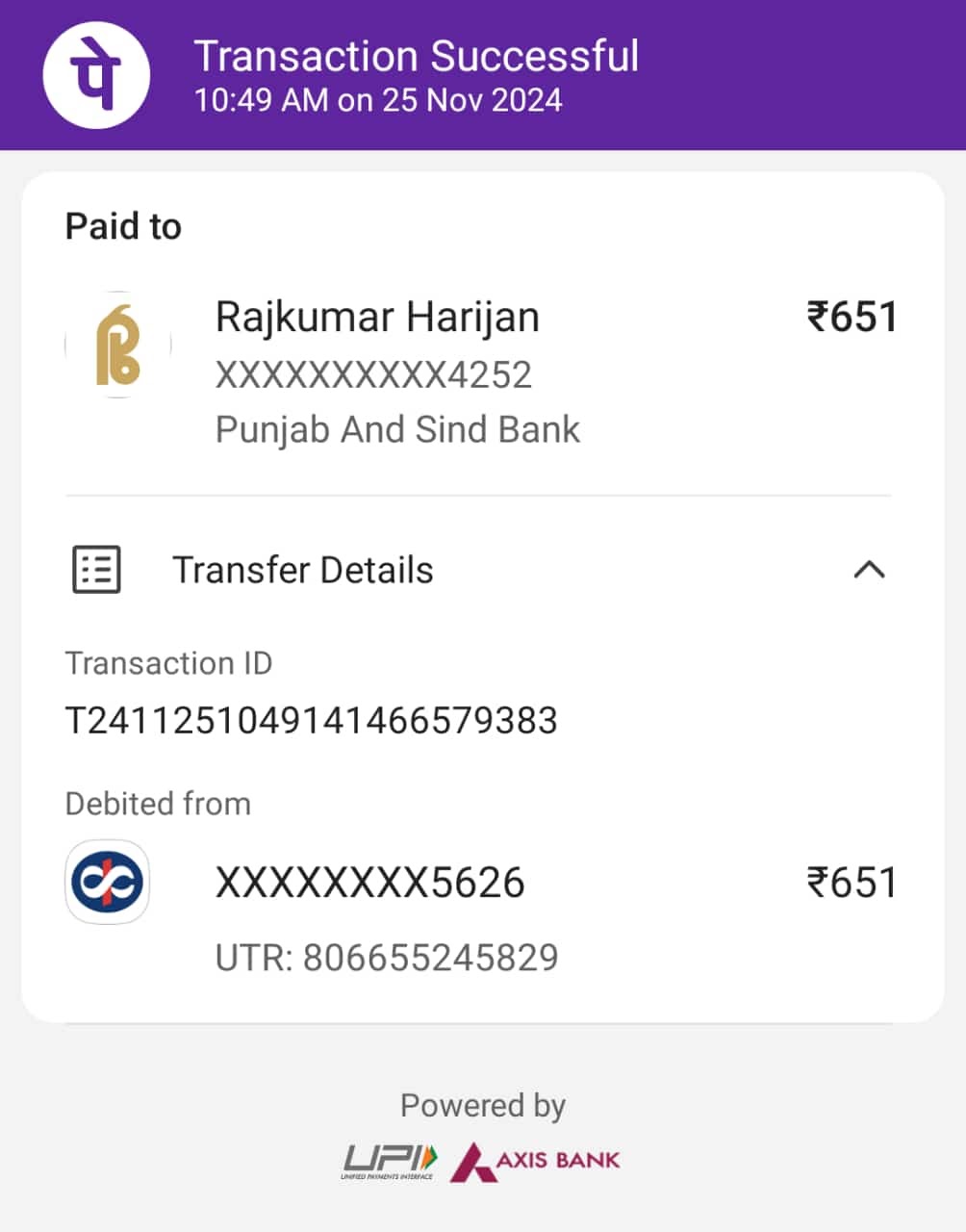

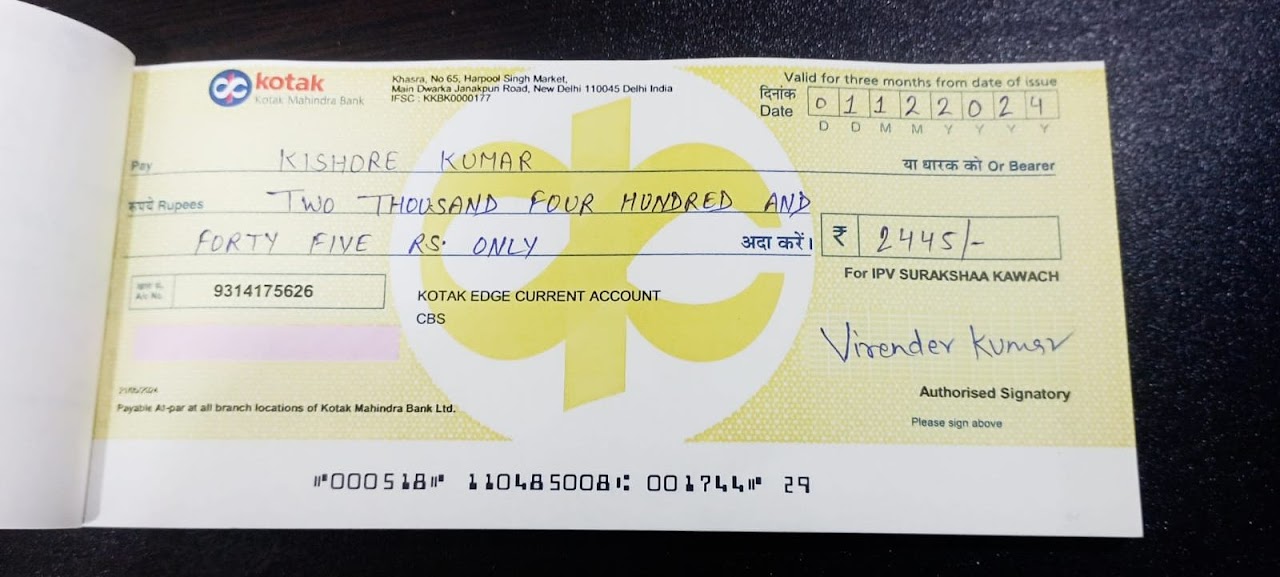

CLICK HERE TO SEE BENEFITS RECEIVED BY EXISTING MEMBERS